5 Things You Need to Know About Big Box Logistics in H1'2026

- Take-up reached 16.8m sq ft in H1 2026, running 4.8% ahead of the same period last year and 19% above the post-Covid average (2023 to 2025). Outside of the Covid years this is the strongest first half on record.

- A further 11.7m sq ft is under offer, of which 45% sits in existing stock, giving us a healthy start going into the second half.

- The DTRE Big Box Vacancy Rate edged up to 7.55%, from 7.3% in Q1. However, Grade A availability has tightened to just 2.6%, down from 2.9%.

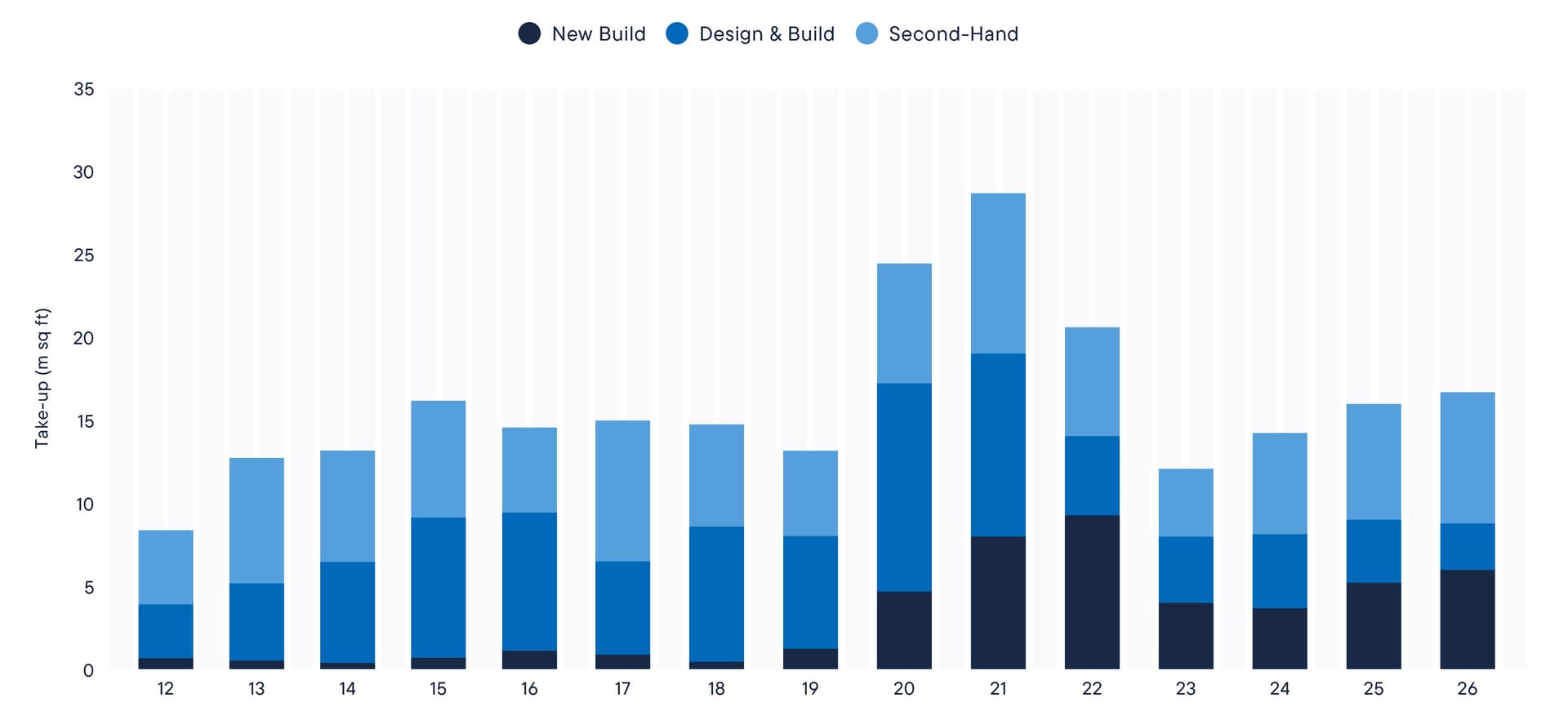

- Second-hand space did the heavy lifting, accounting for 46% of take-up by floorspace, a reminder that there remains a place for the right asset in the right location.

- Capital markets felt the weight of a noisy quarter (the Iran conflict, a renewed energy-led inflation scare and gilts pushing back towards 5%), yet prime income still transacted at strong levels. In an uncertain world, income to a strong covenant is king.

Occupational Market

Take-up of units over 100,000 sq ft reached 9.2m sq ft in Q2 2026 across 34 deals, the stronger of the two quarters this year and enough to lift first-half take-up to 16.8m sq ft. That runs 0.6% ahead of Q2'25 and 29% above the post-Covid quarterly average (2023 to 2025). Outside of the Covid-distorted years this is the strongest first half on record and for a market that has spent much of the last two years being told to brace for a slowdown, that is an impressive return and, furthermore, momentum shows little sign of fading. A further 11.7m sq ft is currently under offer, of which 45% sits in existing stock, demonstrating occupiers' willingness to take well-located 'second-hand' space where the deal stacks up, and giving confidence in a solid H2 to come.

Fig 1. Take-up at H1 by Grade

Source: DXTRE

A retail-led quarter, in a market that keeps rotating

Q2 had a distinctly retail flavour. Retailers accounted for 49% of take-up in the quarter, led by Marks & Spencer (437,000 sq ft, Fradley) and Currys (397,000 sq ft, Newark), with a cluster of online names (Online Home Shop, AO World and a second Amazon commitment at Thurrock) hinting at a return of e-commerce demand. Third-party logistics providers (3PLs) took a further 36%, with Bleckmann (761,000 sq ft, Lutterworth), ID Logistics (673,000 sq ft, Rugby) and CEVA (508,000 sq ft, Derby) all committing to scale.

Big Box is Back

On size, the bigger requirement has returned. The average deal in the first half came in at c.256,000 sq ft, with units of 300,000 sq ft and above accounting for half of all floorspace. After the more cautious commitments of 2022 to 2024, when occupiers were digesting their pandemic-era expansion, sixteen deals of 300,000 sq ft or more completed in the first half.

Which brings us to supply, and the issue that increasingly defines the prime end of the market. The most striking feature of the first half is how much of it was met by second-hand space. Second-hand accounted for 46% of take-up, its highest share in years, and of the sixteen deals over 300,000 sq ft, seven went into existing rather than new stock. That is not necessarily occupier preference but rather a lack of choice.

According to DXTRE (DTRE's proprietary database), across the 300,000 sq ft plus size bands there is now very little genuinely new, ready-to-occupy space. In the 400,000 to 500,000 sq ft band, several of the new build options do not complete until 2027 (WestWorks in Q1 2027 and Stafford 475 in Q2 2027), and at 500,000 sq ft and above the largest available units are overwhelmingly second-hand or sublease space, with Wayfair's 1.2m sq ft at Magna Park offered on assignment and the handful of new build options either already under offer (M1 XL at Sawley) or not yet ready (Panattoni's S915 at Swindon). The genuinely new, large, available box is becoming a rarity.

With the speculative pipeline subdued, just under 6m sq ft due over the next 12 months against a long-run average of c.10.9m sq ft, and developers still constrained by land costs and construction cost inflation, this shortage will not resolve quickly. Expect a supply crunch in prime big box over 300,000 sq ft to become a defining theme through the second half and into 2027, and the consequences are clear enough. Upward pressure on headline rents for the best new product, a tightening of incentives on Grade A space as choice narrows, and more occupiers pushed towards design and build or, when time, and / or capital, is not on their side, well-located second-hand stock.

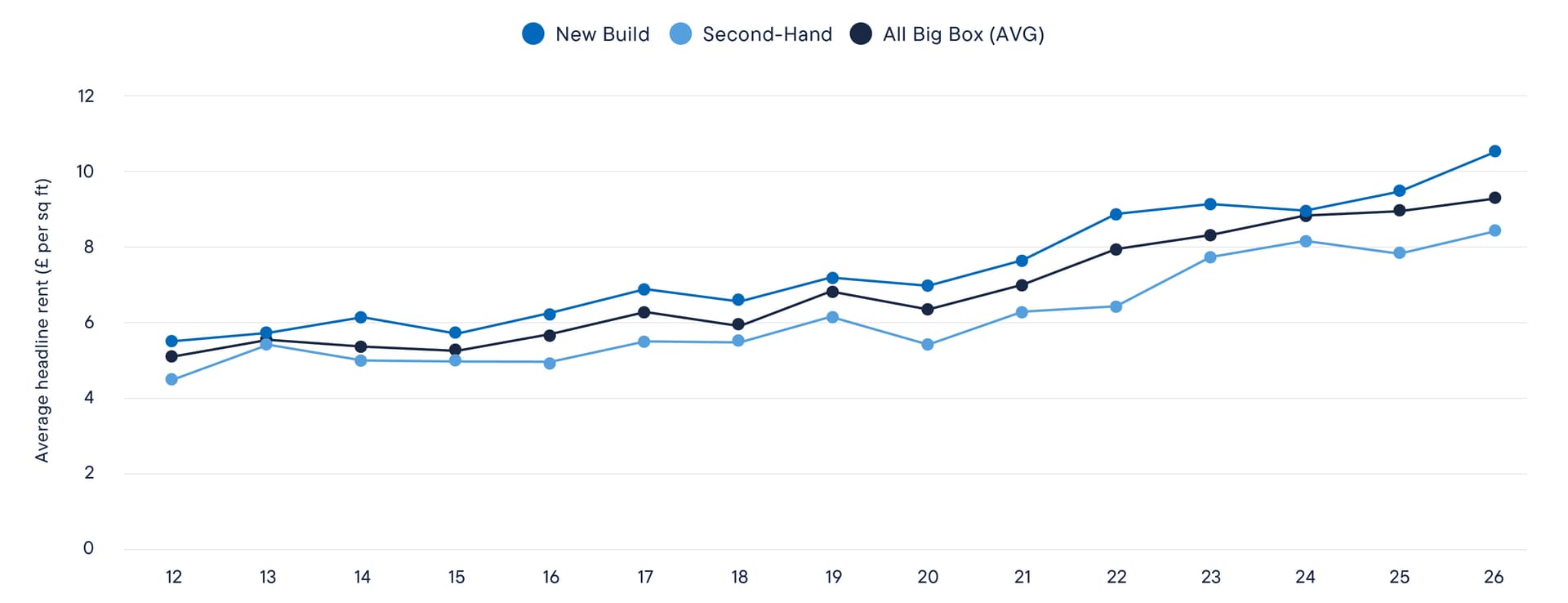

Fig 2. Big Box Headline Rents (Average achieved £ per sq ft, units over 100,000 sq ft.)

Source: DXTRE

Vacancy and Geography

The DTRE Big Box Vacancy Rate edged up to 7.55%, from 7.3% at the end of Q1, but the move is modest and secondary-led. Grade A availability remains tight at 2.6%, down from 2.9% at end Q1'26. The Midlands continues to dominate supply, with the East and West Midlands together accounting for c.36% of the UK's total availability, reaffirming the region's status as the UK's logistics heartland, but the Midlands is a microcosm of the wider supply disconnect seen across the UK. Of the 97 available units in the region, just 5 are new build and larger than 300,000 sq ft and with such little new prime space coming through, we would expect prime vacancy to tighten further even as the headline rate tracks sideways.

Rents firming, polarisation entrenched

In terms of rental growth, the long climb in rents hasn’t dissipated. Average achieved headline rents on big boxes have risen steadily from the c.£5 to £7 per sq ft range that prevailed through the 2010s to c.£9.29 per sq ft so far in 2026, the highest in the series. The gap between new and second-hand is now firmly established, with new build averaging c.£10.53 per sq ft in the first half against c.£8.41 per sq ft for second-hand. At the prime end the tone is firmer still, with £20.00 per sq ft achieved on new build at Gatwick and Amazon paying £17.50 per sq ft at Crawley.

As we move into the second half of the year don't expect the narrative to change too much. There remains a broad, logistics and retail-led demand base, with larger requirements firmly back, and rents on the best space firm and holding. To summarise, at halfway through 2026, the occupational market is in better shape than the prevailing mood music would suggest, and with prime supply thinning, the race-for-space at the top end is only going to intensify.

Capital Markets

If the occupational market spent Q2 quietly getting on with it, the capital markets spent the quarter staring at the headlines.

The conflict involving Iran dragged on through the period, pushing oil higher and reigniting an inflation scare that had looked to be fading. UK CPI held at 2.8% in May, but masked a services reading that jumped to 3.7%, and the 10-year gilt pushed back towards 4.8% in mid-June as the Strait of Hormuz risk premium built. With the Bank of England holding rates steady and the cuts the market had banked on pushed further out, the 'risk-free' rate gave investors little to work with.

For investors, it's a familiar story to previous years. The higher-for-longer narrative with its read across to gilts and swaps kept the bid/ask spread wide and therefore volumes subdued, with several processes paused or recalibrated in some way through the quarter as buyers reset their entry points against a moving geopolitical backdrop.

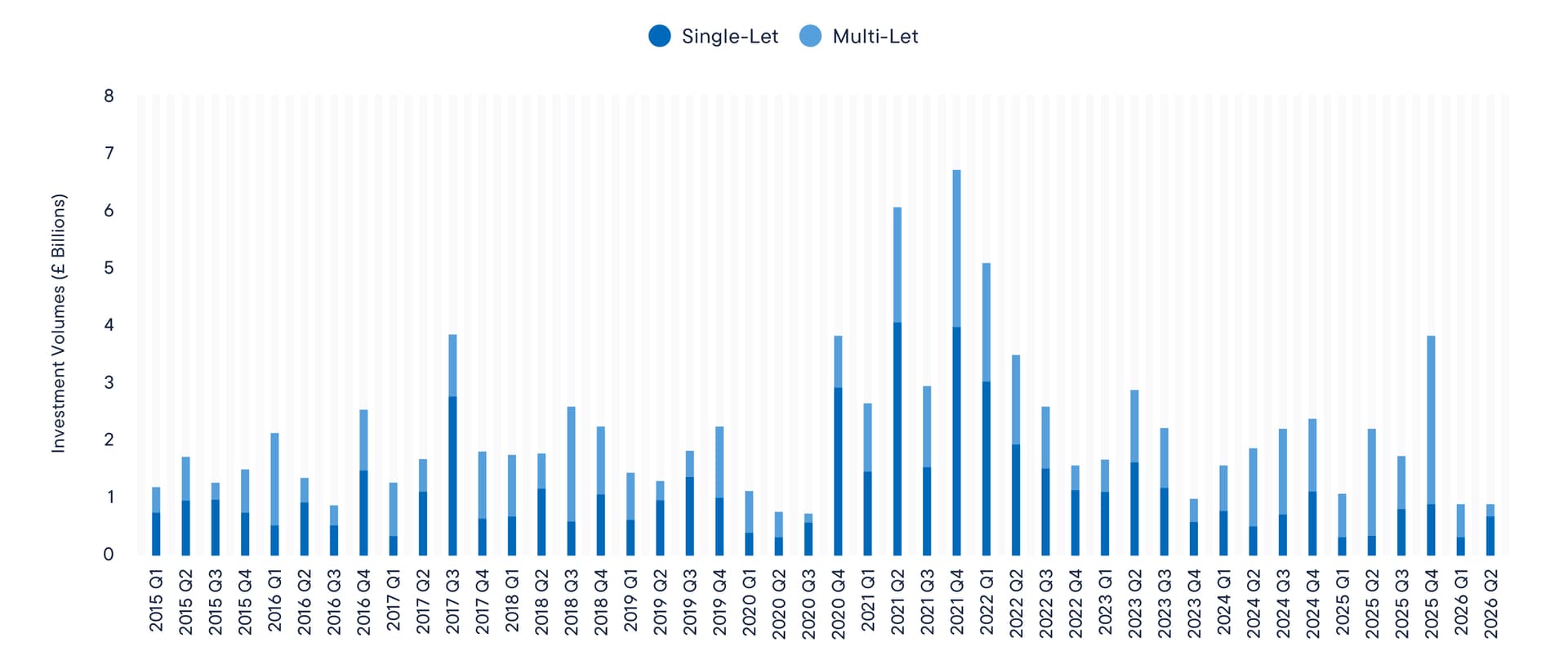

On a provisional basis, £925m of industrial and logistics traded in Q2. The two biggest deals were both portfolios, with ICG acquiring the Springbox Portfolio from Equites Property for c.£200m at a net initial yield (NIY) of 5.26%, EQT's c.£195m acquisition of a 1.55m sq ft package from Tritax (6.10% NIY). The biggest single-let deal was Copley Point's purchase of a 375,000 sq ft B&Q unit in Swindon from Marq Logistics (formerly GLP) for c.£58m, 5.30% NIY. Where the income and the covenant are right, prime pricing has held firm, as demonstrated by the Hines purchase of Heathrow Logistics Park last week for £135m/3.5% NIY, ahead of guide and a tight net initial yield (There is an outstanding rent review that will push the entry yield towards 5% and the acquisition has a reversionary yield of 6%).

Fig 3. Investment Volumes by Quarter

Source: DXTRE

Away from the prime, the picture was softer. The average NIY on big box deals drifted out to c.6.45% in Q2, from c.6.07% in Q1, as secondary and shorter-income assets repriced. Project Sheem (c.£125m, 7.25% NIY) and the Refresco unit at Pontefract (7.51% NIY) sat at the wider end, a fair reflection of where appetite thins out, pricing can drift.

However, there were signs of relief into quarter-end. The interim de-escalation between the US and Iran and the reopening of the Strait of Hormuz pulled oil down to low $70s a barrel and inflation expectations back, and gilts eased towards 4.74%. Whilst there will be no return to 2021-style pricing, the direction of travel late in the quarter is a positive step in the right direction.

Outlook

Expect the second half to be defined by the same two forces that shaped the first.

On the occupational side, a shallow speculative pipeline (well below the c.10.9m sq ft long-run rolling four-quarter average) running into steady, broad-based demand should keep prime vacancy tight and headline rents on new, efficient space firm and the current near 11 million sq ft under offer gives the market a running start.

On capital markets, much rests on Burnham, his choice of Chancellor and the outlook for rates, swaps and gilts. If the late-Q2 easing in oil and inflation expectations holds, and the Bank of England finds room to move later in the year, the bid/ask spread that has frustrated the market for three years should narrow. The anticipated re-organisation of the Local Government Pension Schemes (LGPS) remains a potential source of core capital for single-let logistics, and there remains a significant amount of dry powder still admiring the sector from the sidelines, and buyers with conviction will be rewarded.

DTRE Definitions

Big Box: Unit of 100,000 sq ft +

Take-up: A single-let unit upon which a new lease or occupier freehold purchase has completed (does not include lease renewals/re-gears) and is not conditional upon planning. Deals that have been agreed but remain conditional to planning remain classified as ‘under offer’.

Supply: Currently available. Newly developed units are added to the supply schedule upon reaching practical completion.

Grade A: New or recently refurbished Big Box stock built to modern institutional specification. Typically clear internal height of 12m or more, a modern dock-leveller ratio, 50m+ yard depth, EPC rating of A or A+, and BREEAM Very Good or better. Grade A includes both newly speculatively-built and some ‘second-hand’ units that continue to meet this specification. Built in last 20 years.

Grade B: Functional distribution stock that falls short of Grade A on one or more key specifications — typically lower eaves (c.8–10m), older construction, mid-range EPC ratings (B/C/D), and/or less generous yard and dock provision. Usually older Grade A product that has been overtaken by newer stock, or refurbished units that cannot be brought fully up to modern spec.

Grade C: Older, lower-specification stock, often not originally built as modern distribution warehousing. Typical characteristics include low eaves (<8m), limited yard depth, poor EPC ratings (E or below), and constrained dock provision. Typically candidates for comprehensive refurbishment or redevelopment.

Grey Space: Whole or part-units being actively marketed for sub-lease or assignment by an existing occupier, rather than being offered directly by the landlord. DTRE includes actively-marketed grey space within its total supply schedule, as it represents genuine competition for occupier requirements.